This federal mandate, part of a broader push to modernize payment systems and enhance security, requires all beneficiaries to transition to electronic payments. While most have already enrolled in direct deposit, the final group still receiving paper checks represents a once-in-a-decade opportunity for banks and credit unions to acquire customers, expand financial inclusion, and capture predictable monthly deposits.

The $1B Monthly Opportunity

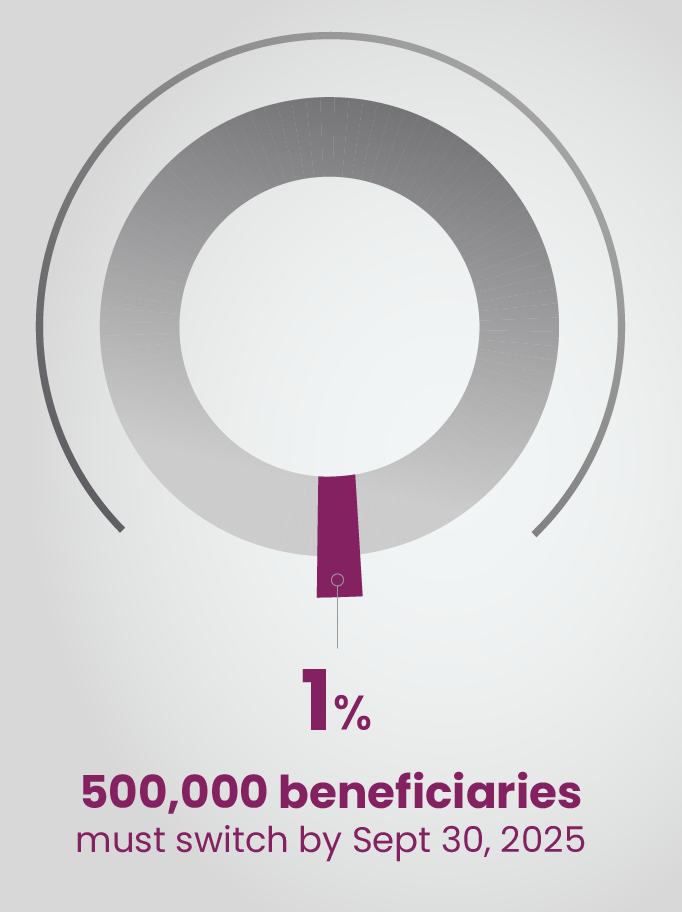

Roughly 1% of beneficiaries — about 500,000 individuals — still receive paper checks. With average benefits ranging from $1,800–$2,000 per month, that translates to over $1 billion in deposits each month that will be redirected into financial institutions.

Who’s Impacted by the Mandate?

The remaining paper check recipients often fall into groups with unique needs:

- Unbanked or underbanked

No traditional checking or savings account. - Elderly or tech-hesitant

Comfortable with paper checks, uncertain about digital tools. - Geographically isolated

Living in rural areas with limited branch or internet access.

Steps in the Implementation Process

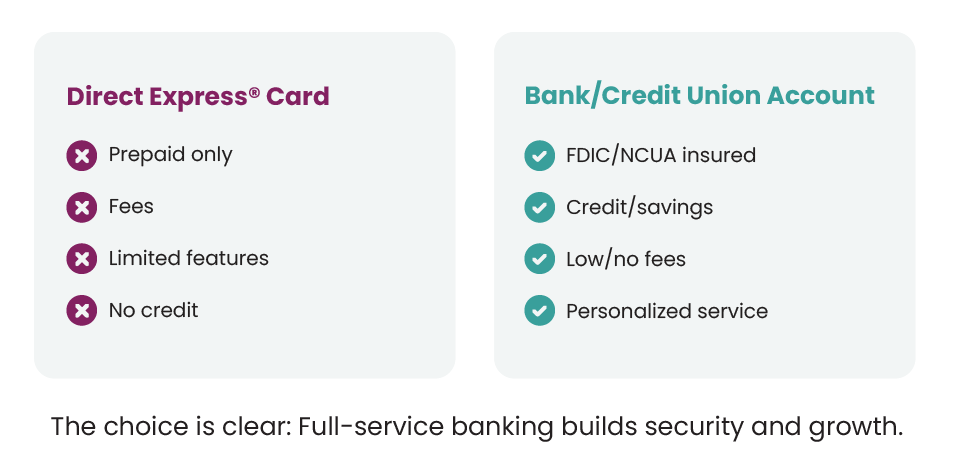

- Direct Deposit - Bank or credit union account.

- Direct Express® Debit Card - A prepaid debit card issued by Comerica Bank.

A Three-Pillar Strategy for Banks & Credit Unions

To win this opportunity, financial institutions must combine education, tailored offerings, and empathetic service.

Outreach & Education

- Partner with community groups and senior centers.

- Provide simplified, multilingual messaging.

- Host in-branch enrollment days.

Tailored Products

- Offer no-cost/low-cost accounts.

- Provide simple digital tools.

- Share financial literacy resources.

Empathetic Service

- Train dedicated specialists.

- Reinforce deposit security with FDIC/NCUA.

How Accelerize 360 Helps Institutions Lead

At Accelerize 360, we turn this mandate into measurable growth — moving from insight to execution inside Salesforce. Our Social Security Digital Mandate Activation is built to help banks and credit unions capture their share of this $1B/month opportunity.

1. Data Cloud Segmentation & Prospect Discovery

- Enrich & Identify:

Use Salesforce Data Cloud to unify first-party data (existing customers, dormant accounts, prior outreach) with third-party demographics (age, geography, income proxies). - Target Modeling:

Build segmentation lists of likely beneficiaries (65+, rural communities, no prior direct deposit enrollment). - Predictive Insights:

Apply lookalike modeling to uncover “hidden” unbanked or underbanked prospects across the database and through local partner lists.

2. Marketing Cloud Journeys: Outreach & Education at Scale

- Multilingual, Multi-Channel Campaigns:

Email, SMS, and phone journeys with clear, simplified messaging that explains the mandate, highlights direct deposit benefits, and walks customers through enrollment. - Community Campaign Kits:

Journey templates to drive attendance at in-branch “Enrollment Days” or workshops. - Progressive Engagement:

Tailor campaigns by digital literacy — paper mail reminders for non-digital, mobile-first nudges for smartphone users.

3. Agentforce: Human + AI Outreach

- AI Prospecting Agents:

Automatically surface qualified leads from CRM (e.g., accounts with ACH activity but no Social Security deposit). - Education Agents:

24/7 AI-powered chatbots to answer FAQs like “How do I sign up for direct deposit?” or “What documents do I need?” - Contact Center Enhancements:

Service Cloud Voice + AI voice agents handle routine enrollment questions, while “Senior Account Specialists” focus on high-touch cases.

4. Accelerated Onboarding & Service

- Guided Enrollment Journeys:

Salesforce checklists help bankers walk seniors through setup step by step. - High-Touch Service Dashboards:

Monitor onboarding progress, flag drop-offs, and ensure follow-through. - Trust Reinforcement:

Automated post-enrollment communications emphasize FDIC/NCUA insurance, fraud protection, and ease of digital tools.

5. The A360 Differentiator: From Knowledge to Action

Anyone can explain the mandate. A360 operationalizes it.

Built directly on Salesforce, so institutions can scale outreach, measure impact (accounts opened, deposits captured), and refine strategy continuously.

Don’t Let the Opportunity Default to Prepaid Cards

The September 2025 mandate represents a $1 billion monthly shift in deposits. Institutions that act now will capture new accounts, expand financial inclusion, and strengthen community trust.Contact us today to discover how Accelerize 360 can help you build smarter, faster, and more scalable solutions with tools like Salesforce Service Cloud Voice, Amazon Connect, and Agentforce.

Accelerize 360 is your partner to make it happen.

Let’s Get Started

Keep Exploring